By Rinki Pandey October 26, 2025

Accepting instant payments in real time isn’t just a nice-to-have anymore—it’s fast becoming the standard customers expect in the U.S. market.

Whether you run a retail store, service business, marketplace, or B2B operation, being able to request, receive, settle, and confirm funds 24/7/365 can accelerate cash flow, reduce cart abandonment, and unlock new customer experiences.

This comprehensive guide (U.S.-focused) walks you through the instant-payment rails (FedNow, RTP, push-to-card), key compliance and fraud controls, integration choices, pricing models, and a practical rollout plan.

We’ll also cover industry-specific playbooks, KPIs to track, and FAQs so you can confidently implement instant payments for real-time results.

What “Instant Payments” Really Mean for U.S. Businesses

When U.S. merchants talk about instant payments, they typically mean funds move and become available to the receiver within seconds, with finality and immediate confirmation.

That’s different from traditional card “authorizations” that still settle in batches later, and different from Same Day ACH, which is faster than standard ACH but still processed in windows and only on business days.

The promise of instant payments is deterministic cash flow: you know in real time that money has moved. That in turn reduces operational friction—no waiting for nightly batches, fewer painful reconciliation delays, and less reliance on manual workarounds.

For customers, instant confirmation reduces anxiety and improves satisfaction at checkout or when paying invoices. For owners, always-on rails can compress the order-to-cash cycle, improve inventory turns, and support new use cases like instant refunds, just-in-time disbursements, or pay-on-delivery.

Practically, instant payments live across several rails in the U.S.—not just one. You’ll evaluate bank-to-bank rails (FedNow, RTP) alongside push-to-card (Visa Direct, Mastercard Send) and wallet ecosystems.

The right blend depends on your ticket size, audience, risk profile, and the payment experiences you want to deliver, but the goal is the same: consistent, reliable, real-time movement of money paired with strong controls.

The Core U.S. Instant-Payment Rails You Should Know

Modern instant payments in the U.S. span three families of rails, each with strengths:

1) Bank-to-bank instant rails (24/7/365)

- FedNow® Service is the Federal Reserve’s instant-payment infrastructure that enables participating U.S. depository institutions to clear and settle payments in real time, around the clock.

It launched on July 20, 2023, and is designed to support a wide array of instant use cases through participating banks and credit unions. - RTP network by The Clearing House is another real-time payments platform available to federally insured depository institutions, built for 24/7/365 irrevocable credit transfers and instant confirmation.

Adoption continues to expand, already reaching a large footprint of accounts via participating institutions.

2) Push-to-card (near-real-time disbursements to debit/prepaid)

- Visa Direct supports pushing funds to eligible debit and prepaid cards using card network messaging (e.g., Original Credit Transaction/OCT) to deliver funds quickly for many use cases like payouts, refunds, and gig worker earnings.

- Mastercard Send offers similar capabilities for near real-time payments to card accounts, widely used for B2C disbursements and P2P flows.

3) Wallet and app ecosystems

Consumer-facing wallets (PayPal, Venmo, Cash App, Apple Cash) can deliver a near-instant user experience, especially wallet-to-wallet. For merchants, the “instant” aspect can depend on settlement methods from the provider to your bank account (some offer instant transfer options for a fee).

Wallets can broaden acceptance and conversion, but you should weigh fees, brand alignment, chargeback policies, and reconciliation effort. In many stacks, wallets complement bank-to-bank or push-to-card rails rather than replace them.

These rails are not mutually exclusive. Most businesses adopt a multi-rail approach to meet customer preferences, optimize costs, and ensure redundancy.

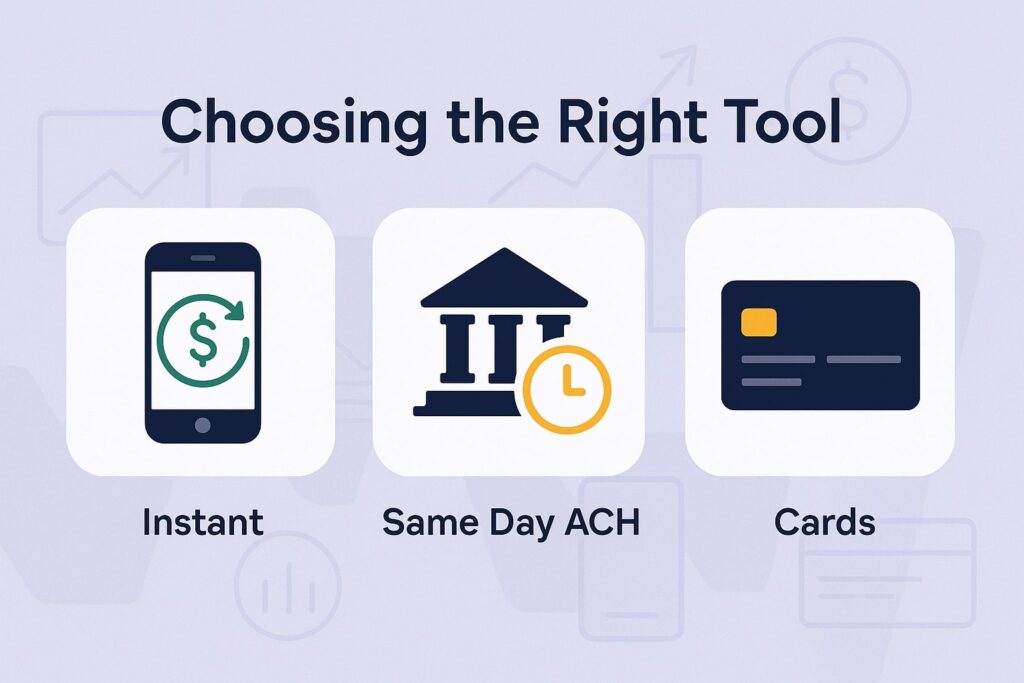

Instant vs. Same Day ACH vs. Cards: Choosing the Right Tool

Instant rails (FedNow, RTP, push-to-card) move money in seconds with immediate confirmation and, for bank rails, 24/7/365 availability. They’re best for time-sensitive flows: on-demand payouts, instant refunds, after-hours collections, high-urgency invoices, or pay-on-delivery.

Same Day ACH is a faster version of ACH that processes within defined windows on business days; funds post the same day (within limits), but it’s not 24/7/365 and lacks the real-time confirmation and finality characteristics of instant rails.

Nacha has continued modernizing windows and limits, and has explored adding a fourth daily window, but ACH remains batch-based and tied to business-day schedules.

Cards are ubiquitous and optimized for consumer checkout, but settlement to the merchant is T+1 or longer, and chargebacks follow card-network rules.

In contrast, instant payments over bank rails are credit-push with immediate finality, which can reduce certain dispute scenarios while introducing new operational considerations (e.g., refund flows, messaging, and ISO 20022 remittance data mapping).

Compliance & Risk Fundamentals for Instant Payments

Moving money instantly requires robust controls. Start with KYC/KYB for customers and merchants (if you’re a platform/marketplace), verifying identity, beneficial ownership, and risk signals at onboarding and periodically thereafter.

Layer AML/CFT screening, sanctions checks (OFAC), and continuous monitoring to detect unusual payment patterns. For consumer protections, understand how Reg E applies to electronic fund transfers and error resolution for unauthorized transactions in consumer accounts; your obligations differ by rail and role (e.g., bank vs. third-party provider).

Document clear refund and dispute policies for instant rails, which typically operate as irrevocable credit transfers—meaning you won’t rely on card-style chargebacks and should provide customer-friendly remediation (e.g., instant refunds via the same rail, or a push-to-card fallback).

Build a transaction-risk program tailored for real time: velocity controls, device fingerprinting, geo/IP signals, behavioral analytics, and step-up authentication for high-risk events.

Finally, ensure data security (PCI DSS when you handle cards, SOC 2 for platforms/processors, encryption, secure key management) and retain messaging/remittance data per your retention schedule and regulator expectations.

The Merchant Readiness Checklist (People, Process, Platform)

To go live with instant payments smoothly, anchor your plan around three pillars:

- People: Assign an executive sponsor (CFO/COO/Head of Payments) and a cross-functional tiger team—payments product owner, treasury lead, finance controller, risk/fraud manager, compliance officer, customer support lead, and engineering.

Clarify SLAs for settlement posting, exception handling, and refund timing. Train support teams to explain instant status, confirmation codes, and refund policies. - Process: Map your full payment lifecycle: initiation, authentication, confirmation, settlement posting, reconciliation, refund/credit, dispute handling, exception queues (e.g., rejects, returns, timeouts for a given rail), and communications (receipts, notifications).

Define fallback paths (e.g., if an RTP attempt fails, offer FedNow or push-to-card) and cutover rules. Create playbooks for varied scenarios—after-hours payouts, large-ticket invoices, or micro-transactions. - Platform: Choose your enablement route: (1) bank-direct connections, (2) payments service providers (PSPs) or gateways with instant rails, or (3) orchestration platforms that route across multiple rails. Confirm your rails (FedNow/RTP/push-to-card) and product features (request-for-payment, instant refunds).

Ensure API and webhook coverage, idempotency keys, message signing, and robust observability (traces, metrics, logs). Verify ledgering and reconciliation are real-time aware, not batch-only.

Integration Options: Bank Direct vs. PSP vs. Orchestration

- Bank Direct: If you have a strong treasury relationship and engineering resources, bank-direct connections to FedNow and/or RTP can give you cost control, transparency, and custom workflows.

You’ll manage message specifications (often ISO 20022), reference fields, and schema mapping. This path suits enterprises with dedicated payments engineering and the desire to tune performance and costs. - Payments Service Provider (PSP): PSPs abstract away bank connectivity and offer drop-in SDKs or unified APIs. They can also blend instant payments with cards, ACH, and wallets, giving you a single settlement and reporting layer.

Evaluate PSP coverage of FedNow, RTP, and push-to-card along with features like Request for Payment (RfP), instant payouts, account validation, and risk tools. PSPs can accelerate time-to-market while adding a margin to costs. - Payments Orchestration: Orchestrators sit between you and multiple providers, dynamically routing traffic based on success rate, cost, or rail availability.

For instant payments, orchestration helps with circuit breakers and intelligent fallback (e.g., RTP → FedNow → push-to-card), improving resilience and authorization success. Orchestration adds complexity but boosts bargaining leverage and uptime.

Pricing, Costs, and the Business Case

Expect three cost buckets: per-transaction fees (by rail/provider), platform fees (monthly or per-feature), and fraud/compliance investments (tools, reviews, charge-off reserves). Bank direct pricing for FedNow/RTP can be efficient at volume; PSP pricing trades a margin for speed-to-market.

Push-to-card often adds a per-payout fee and, sometimes, a percentage component—value is strongest for instant refunds and disbursements where customer delight and retention outweigh cost.

To model ROI, quantify: cart conversion uplift from instant options; abandoned invoice recovery when buyers can pay after hours; support cost reductions from fewer “where’s my refund?” tickets thanks to immediate confirmations; working-capital improvements from faster cash application; and marketplace take-rate opportunities enabled by instant seller payouts.

Don’t just compare per-transaction fees—compare outcome metrics (net revenue, DSO, refund ETA, NPS).

Customer Experience: Designing for Trust and Speed

A great instant payments UX reduces friction and drives adoption:

- Choice with clarity. Offer a short list of rails with plain-language labels (e.g., “Pay now from your bank (instant)” versus jargon).

- Real-time feedback. Show progress states: “Initiated → Confirmed → Funds Available,” with timestamps and reference IDs.

- Authentication that fits the moment. Keep low-risk payments fast (e.g., passkeys, 3DS for cards where needed, bank-auth for account-to-account), and step up for high-risk.

- Refund transparency. If you support instant refunds, make that promise explicit (“Instant refund back to your bank 24/7”).

- Receipts and messaging. Include rail, last four of the destination, amount, time, and an inquiry link. Customers should feel in control, especially after hours.

- Accessibility and mobile-first. Instant is often mobile-initiated; ensure tap-friendly UI, clear contrast, and strong error messaging.

Industry Playbooks for Instant Payments

- Retail & eCommerce: Use instant bank pay for high-ticket items and instant refunds to reduce post-purchase anxiety. Combine real-time stock allocation with confirmed funds to release inventory immediately. Promote instant as a perk in loyalty programs.

- Services & Field Operations: Let technicians generate instant payment requests in the field with QR codes or links, then confirm receipt to unlock job completion steps. Offer instant partial refunds or adjustments on-site to defuse disputes.

- Marketplaces & Platforms: Recruit sellers with instant payouts (on-demand, 24/7) to their bank or debit card. Add programmatic RfP for invoice settlement. Implement reserve logic and velocity checks per seller risk tier.

- B2B & Professional Services: Use instant rails for pay-on-delivery freight, milestone-based construction draws, or emergency procurement. Map remittance data (ISO 20022 fields) to your ERP to automate cash application and match PO/Invoice/Payment instantly.

Fraud, Disputes, and Refunds in a Real-Time World

Real-time speed compresses your decision window. Build layered defense:

- Identity proofing & linking: Verify that a customer, device, funding account, and destination are a coherent, low-risk cluster.

- Behavioral analytics: Look for unusual send-patterns, device changes, and late-night spikes. Apply velocity limits and cooling periods for new payees.

- Confirmation & receipts: Instant rails produce confirmations; include them in receipts and internal logs.

- Customer education: Make payee names unambiguous, show merchant logos in banking apps where supported, and warn about scams.

- Refund mechanics: Because many instant transfers are irrevocable, your internal refund workflow is essential. Provide instant refunds where possible to encourage honest reporting and reduce support load.

- Post-transaction monitoring: Real-time doesn’t end at confirmation—monitor for first-party fraud, mule activity, and synthetic identities.

Selecting Providers: A Practical Evaluation Matrix

When choosing a bank, PSP, or orchestration partner for instant payments, score vendors on:

- Rail coverage & capabilities: FedNow send/receive, RTP send/receive, RfP support, push-to-card breadth, wallet breadth, instant refunds.

- Availability & performance: 24/7/365 SLA, historical uptime, p95/p99 latency, failover regions, and queued-message handling.

- Risk & compliance: Built-in KYC/KYB, sanctions screening, transaction monitoring, rules engine, case management, audit trails.

- Developer experience: API clarity, SDKs, webhook reliability, idempotency, sandbox fidelity, versioning, and change-log discipline.

- Treasury & reconciliation: Real-time ledger, intraday reporting, ISO 20022 mapping, ERP connectors, statement formats (BAI2/ISO camt).

- Commercials: Pricing transparency, volume tiers, pass-through network fees, statement detail, and contract flexibility.

- Support & roadmap: 24/7 support, named CSM, migration help, feature pipeline for instant rails.

Implementation Roadmap: From Pilot to Scale

- Phase 1 – Discovery & Design: Document use cases (instant checkout, instant payout, instant refund). Choose your rails and fallback logic. Define risk policies and compliance checks. Update terms and customer comms.

- Phase 2 – Build & Integrate: Wire up APIs, webhooks, and your ledger. Implement RfP where relevant. Add real-time dashboards for ops, finance, and risk. Prepare regression tests for time-of-day edge cases (nights, weekends, holidays).

- Phase 3 – Pilot: Start with one use case and a small segment. Measure latency, success rate, refund times, and support tickets. Run A/B tests on UX copy for instant payments to confirm adoption.

- Phase 4 – Scale & Optimize: Expand to more segments and introduce orchestration and smart-routing. Optimize costs by rail and introduce instant loyalty perks (e.g., “instant refund eligibility”).

KPIs That Prove Instant Payments Are Working

Track both speed and business outcomes:

- Authorization/success rate by rail and time of day.

- End-to-end latency: initiation → confirmation → funds availability.

- Instant refund ETA and refund adoption rate.

- Collections lift (invoice past-due reduction) and DSO improvement.

- Checkout conversion and cart abandonment deltas when instant options are shown.

- Support tickets related to payment status or refund timing.

- Fraud rate and false-positive declines after tuning.

- Rail mix & cost per transaction vs. revenue lift.

U.S. Regulatory & Network Nuances (High-Level)

In the U.S., your obligations vary by role (bank, sponsor bank customer, PSP, marketplace) and rail. For bank-to-bank instant rails, study network rules and message formats (ISO 20022) and align your customer terms and refund policies with the nature of irrevocable credit transfers.

For push-to-card, adhere to card-network compliance rules (e.g., OCT eligibility, message requirements) and brand-usage guidelines. Understand how Reg E may apply for consumer EFTs and your error-resolution timelines; coordinate with your bank/PSP on responsibilities, disclosures, and operational playbooks.

For Same Day ACH, monitor Nacha rule changes, including proposals to add windows and evolving dollar limits and risk frameworks; ACH is improving, but it is not the same as 24/7/365 instant payments.

Real-World Use Cases Enabled by U.S. Instant Rails

- Instant payouts to sellers, drivers, or contractors—improving retention with on-demand earnings via bank-to-bank or push-to-card. Visa Direct and Mastercard Send are common for debit-card payouts at scale.

- Invoice settlement after hours using RTP or FedNow with real-time confirmation and rich remittance data for automatic cash application.

- Instant refunds at the point of return to delight customers and cut support costs—implemented via push-to-card or bank-to-bank instant credit.

- Request for Payment (RfP) flows that let you send a payment request and receive immediate, confirmed funds from the buyer’s bank account through compatible instant rails. (RfP availability varies by provider and institution on FedNow/RTP.)

Instant Payments and Settlement/Treasury Management

“Instant” doesn’t replace sound treasury practice. Configure intraday sweeping to consolidate funds from your instant accounts into operating accounts, respecting minimum balances. Align cutoffs for vendor payments and payroll to make the most of 24/7/365 availability while controlling fees.

Ensure your ERP/ledger can post and reconcile in real time based on rail confirmations and that you can produce intraday cash-position reports. For marketplaces, design reserve and rolling settlement logic that uses instant rails for low-risk payouts while holding a portion for potential refunds or risk review.

Accessibility, Inclusion, and Customer Trust

Use instant payments to improve access for customers who prefer paying from a bank account rather than a credit card. Provide fee transparency and disclose any instant transfer fees if you pass them on. Offer alternative rails to accommodate customers whose financial institutions don’t yet support a given instant network (coverage is growing but not universal).

Early FedNow adoption started with a group of participant institutions and continues to expand; similarly, RTP participation grows over time. Designing a multi-rail stack ensures no customer is stranded by any single network’s coverage.

Frequently Asked Questions

Q1) Are FedNow and RTP the same thing?

Answer: No. FedNow is operated by the Federal Reserve, while RTP is operated by The Clearing House. Both are 24/7/365 instant bank-to-bank rails, but they are separate networks and not interoperable today.

Your bank or provider may support one or both; many businesses use multiple rails for coverage and redundancy.

Q2) Do instant payments work nights, weekends, and holidays?

Answer: Yes—one of the prime benefits of instant payments over FedNow and RTP is round-the-clock operation with immediate confirmation. Push-to-card payouts can also be near real time, depending on card/network and receiving institution.

Q3) Is Same Day ACH the same as “instant”?

Answer: No. Same Day ACH is batch-based with processing windows on business days. It’s significantly faster than standard ACH but not real time and not 24/7/365. Instant rails move money within seconds with immediate confirmation.

Q4) What use cases fit push-to-card vs. bank-to-bank instant rails?

Answer: Use push-to-card (Visa Direct, Mastercard Send) for consumer or contractor payouts to debit/prepaid cards—ideal for earnings, tips, insurance claims, gaming withdrawals, or instant refunds to a card.

Use FedNow/RTP for account-to-account payments, B2B invoices, and disbursements where you want remittance data and bank-level messaging. Many businesses deploy both.

Q5) How do I handle chargebacks or disputes on instant rails?

Answer: Bank-to-bank instant payments are credit-push and typically final once posted, so card-style chargebacks don’t apply in the same way. You’ll rely on strong authentication, fraud controls, and merchant-friendly instant refunds and customer support. Your bank/provider agreement and network rules govern exceptions.

Q6) What’s the fastest way to pilot instant payments?

Answer: Use a PSP that already supports RTP/FedNow and push-to-card, integrate their SDKs, and launch a tightly scoped use case (e.g., instant refunds or instant payouts to sellers). Prove lift, measure KPIs, and then expand to checkout and invoices with orchestration and fallback routing.

Step-by-Step Quick Start (Actionable Checklist)

- Pick the first use case (instant refund, instant payout, instant invoice collection).

- Select your enablement (bank direct vs. PSP vs. orchestration).

- Confirm rail coverage (FedNow/RTP send/receive, push-to-card; ask about RfP).

- Implement risk controls (KYC/KYB, sanctions, rules, device intelligence, velocity, step-up auth).

- Integrate & test (APIs, webhooks, ledgering, idempotency, monitoring, fallback routing).

- Train support & finance (instant status, confirmations, refund workflows, reconciliation).

- Pilot with metrics (success rate, latency, refund ETA, support tickets, conversion lift).

- Scale (expand rails, add wallets, optimize cost by rail, introduce instant-eligibility perks).

Conclusion

In the U.S., instant payments let you meet customers where they are—on mobile, after hours, and expecting immediate confirmation. By blending FedNow and RTP with push-to-card and selective wallet options, you can deliver a resilient, multi-rail experience that improves conversion, accelerates cash flow, and reduces operational drag.

The keys are disciplined planning, robust compliance and fraud controls, great UX, and a phased rollout guided by clear KPIs. Start small—instant refunds or instant payouts—prove the value, then scale across your checkout and invoicing flows.

With the right partners and playbooks, instant payments can become one of the most trusted, high-impact parts of your customer experience and your bottom line.